Managing risk is fundamental to trading and investing. Among the sophisticated techniques used by options traders, delta-neutral strategies stand out as a core method for reducing exposure to price fluctuations in underlying assets. This article provides a comprehensive yet accessible explanation of what delta-neutral trading means, how it works in practice, and its advantages and drawbacks.

What is a Delta-Neutral Strategy?

A delta-neutral strategy seeks to balance positive and negative deltas across a portfolio so that the net delta is effectively zero. In simple terms, the goal is to ensure that small price movements in the underlying asset do not significantly impact the overall value of the portfolio.

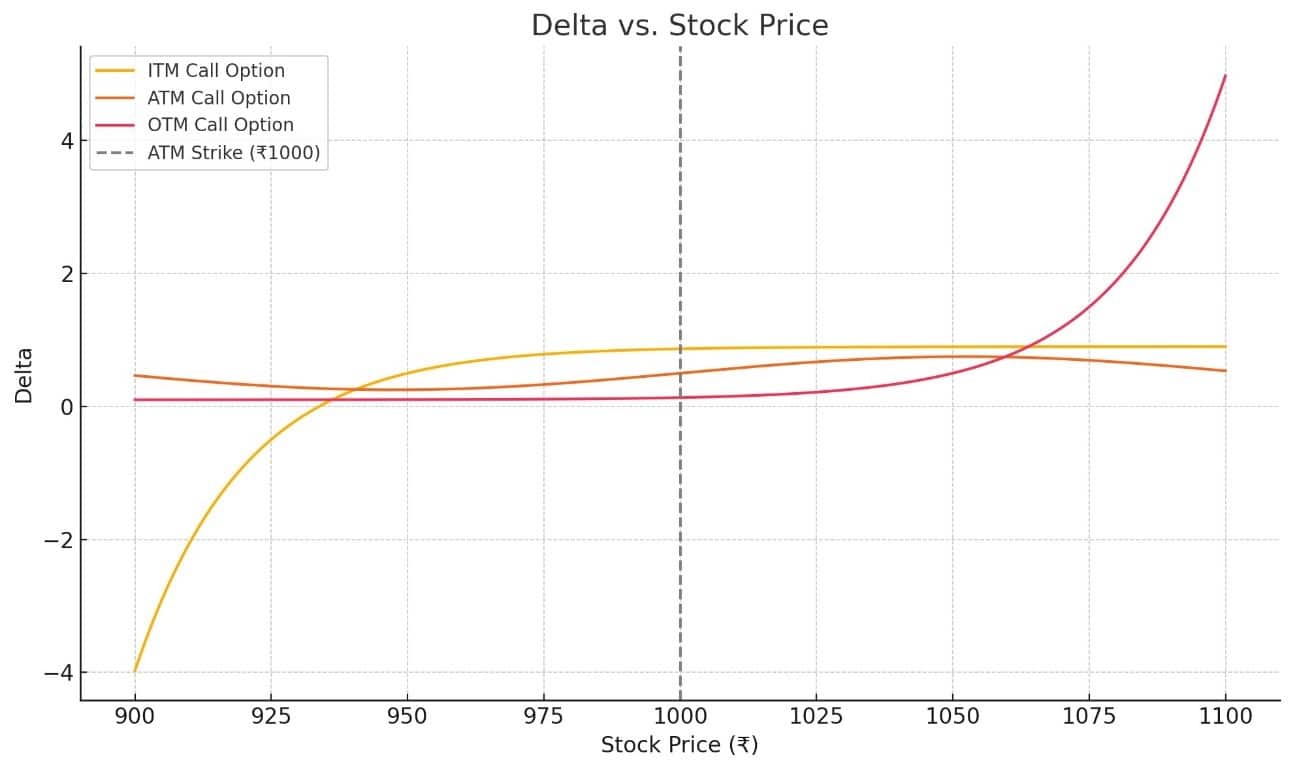

To understand why this matters, one must first grasp the concept of delta itself. Delta is one of the key “Greeks” in options trading. It measures the sensitivity of an option’s price to changes in the price of the underlying asset.

For example, a call option with a delta of 0.25 implies that for every ₹1 increase in the underlying asset’s price, the option’s price is expected to increase by ₹0.25.

Positive, Negative, and Neutral Delta

Depending on the positions held, a portfolio can be:

- Positive Delta: The portfolio benefits when the underlying asset price rises. This is typical for long call options or long stock positions.

- Negative Delta: The portfolio benefits when the underlying asset price falls. This often results from holding long put options or shorting stocks.

- Neutral Delta: Gains or losses from small price movements in the underlying asset are offset, keeping the portfolio stable.

Traders who pursue delta neutrality aim to eliminate directional risk, allowing them to focus on other factors, such as time decay (theta) or changes in implied volatility (Vega), which also significantly influence options pricing.

How Delta-Neutral Strategies Work?

Consider the following example:

Suppose a trader owns a long position of 200 shares in Company X, each trading at ₹100. This position carries a total delta of +200. If the trader wishes to hedge against short-term downside risk while retaining long-term exposure, they could purchase put options to offset this positive delta.

Assuming an at-the-money put option on Company X has a delta of -0.50, buying one contract (representing 100 shares) would contribute -50 delta to the portfolio. To neutralize a +200 delta position, the trader would purchase four such put contracts:

Total delta of puts = 4 × (-0.50 × 100) = -200

The net delta of the combined position becomes zero:

+200 (stock) + (-200) (puts) = 0

In this delta-neutral position, small price movements in Company X’s stock price will not substantially affect the overall portfolio value. However, this balance is not permanent. As the stock price moves, the delta of the options changes due to a factor known as gamma, necessitating periodic adjustments—a process known as dynamic hedging.

Likewise, if an option has a delta of zero and the share price increases by ₹1, the option’s price remains unaffected (typical of deep out-of-the-money call options). If an option has a delta of 0.5, its price will increase by ₹0.50 for every ₹1 increase in the underlying share price. This is calculated as follows:

₹1 price change × delta of 0.5 = ₹0.50 change in option price

Instruments Used in Delta-Neutral Hedging

Delta-neutral strategies can involve various combinations:

- Stock and Options: As in the example above, owning shares while holding options positions to offset delta exposure.

- Calls and Puts: Traders might combine calls and puts to create neutral exposure. For instance, buying a call with a delta of +0.50 and a put with a delta of -0.50 can yield a net zero delta, known as a straddle.

- Synthetic Positions: Traders may construct synthetic positions mimicking the payoff of another instrument to achieve delta neutrality.

These strategies enable traders to isolate and speculate on non-directional factors such as volatility or time decay without taking a directional view on the underlying asset.

Benefits and Challenges of Delta-Neutral Strategies

Advantages:

- Reduces exposure to small price fluctuations in the underlying asset.

- Enables traders to profit from other variables like volatility changes or time decay.

- Offers flexibility in managing complex portfolios.

Drawbacks:

- Requires ongoing monitoring and adjustments due to gamma risk.

- May incur significant transaction costs from frequent rebalancing.

- Large, unexpected market moves can still expose the trader to risks beyond the neutralized range.

Delta Hedging as a Risk Management Tool

Delta hedging specifically refers to the process of adjusting a portfolio’s positions to maintain a delta-neutral state. For instance, if the underlying asset rises, the delta of the options in the portfolio may increase, requiring the trader to sell shares or buy additional options to bring the net delta back to zero.

This is not merely a one-time adjustment but a continuous process. Delta is a dynamic measure, and maintaining neutrality can be demanding both operationally and financially.

Profit Potential in Delta-Neutral Trading

While delta-neutral strategies can shield traders from price movements, they are not purely defensive tools. Many traders use these techniques to:

- Capture profits from time decay as options lose value over time.

- Exploit anticipated changes in implied volatility.

- Manage complex multi-leg options trades where directional exposure is undesirable.

For instance, a trader might sell an options straddle (selling both a call and a put at the same strike price) in anticipation of low volatility. In such a trade, being delta neutral initially ensures that small market movements do not erode the position’s profitability while the trader earns the premium from time decay.

Final Thoughts

Delta-neutral strategies represent one of the most significant tools in the arsenal of advanced options traders. By balancing positive and negative deltas, traders can manage risk, focus on volatility opportunities, and navigate complex market conditions.

However, delta neutrality is not a set-and-forget solution. Market movements, volatility changes, and the passage of time all influence a portfolio’s delta, demanding careful attention and dynamic management.

For traders willing to commit the time and resources required, delta-neutral strategies offer both powerful hedging capabilities and sophisticated avenues for non-directional profits.

For more information, contact RMoney at 0562-4266600 / 0562-7188900 or email us at askus@rmoneyindia.com

Disclaimer:-Investments in the securities market are subject to market risks. This content is for Educational purposes only and does not constitute financial advice.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Journey

Tracing our growth and milestones over time.

Journey

Tracing our growth and milestones over time.

Mission & Vision

Guided by purpose, driven by long-term vision.

Mission & Vision

Guided by purpose, driven by long-term vision.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Management

Experienced leadership driving strategic financial excellence.

Management

Experienced leadership driving strategic financial excellence.

Credentials

Certified expertise with trusted industry recognition.

Credentials

Certified expertise with trusted industry recognition.

Press Release

Latest company news, updates, and announcements.

Press Release

Latest company news, updates, and announcements.

Testimonials

Real client stories sharing their success journeys.

Testimonials

Real client stories sharing their success journeys.

7 Reasons to Invest

Top benefits that make investing with us smart.

7 Reasons to Invest

Top benefits that make investing with us smart.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

Our Technology

Advanced tools enabling efficient online trading.

Our Technology

Advanced tools enabling efficient online trading.

Blog

Stay updated with expert insights, market trends, and trading strategies through our informative blogs.

Blog

Stay updated with expert insights, market trends, and trading strategies through our informative blogs.

Video

Learn visually with easy-to-understand videos covering trading concepts, tips, and market analysis.

Video

Learn visually with easy-to-understand videos covering trading concepts, tips, and market analysis.

Podcast

Tune in to insightful discussions and expert opinions anytime, anywhere.

Podcast

Tune in to insightful discussions and expert opinions anytime, anywhere.

Telegram Community

Be part of an active trader community sharing ideas, updates, and market opportunities in real-time.

Telegram Community

Be part of an active trader community sharing ideas, updates, and market opportunities in real-time.

WhatsApp Updates

Get instant alerts, key market updates, and important notifications directly on WhatsApp.

WhatsApp Updates

Get instant alerts, key market updates, and important notifications directly on WhatsApp.

Financial Calculators

Plan your trades, margins, and returns efficiently with our smart calculation tools.

Financial Calculators

Plan your trades, margins, and returns efficiently with our smart calculation tools.

Marketplace

Discover curated tools, strategies, and services designed to enhance your trading experience.

Marketplace

Discover curated tools, strategies, and services designed to enhance your trading experience.

Feedback

Share your suggestions or concerns to help us improve your experience.

Feedback

Share your suggestions or concerns to help us improve your experience.

Downloads

Access important forms, software, and documents in one place.

Downloads

Access important forms, software, and documents in one place.

Locate Us

Find the nearest RMoney branch or service center quickly.

Locate Us

Find the nearest RMoney branch or service center quickly.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Account Modification

Update personal or bank details linked to your trading account.

Account Modification

Update personal or bank details linked to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.

Authorised Person Partner with us as an Authorised Person to grow your financial business.

Authorised Person Partner with us as an Authorised Person to grow your financial business.

Refer & Earn

Invite friends and earn rewards every time they trade with us.

Refer & Earn

Invite friends and earn rewards every time they trade with us.