Home » Blogs » Mutual Funds » Mutual Funds vs. Direct Equity: Which Builds Wealth Faster?

Investing in India has come a long way from a time when a mere fraction of households had a direct equity stake in the Indian capital markets, and now that many retail investors have access to systematic investments in mutual funds, there is more choice for the investor today than ever before. But with choice comes the question: should the investor invest directly in stocks or invest through mutual funds? And perhaps the more critical question is which alternative provides the quickest means to build wealth?

If you had started a ₹10,000 monthly SIP in 2005, chances are you’d already be sitting on more than ₹1 crore today. But if you had picked winners like HDFC Bank, Infosys, or Reliance back then, your wealth would have grown even faster.

That’s the big question Indian investors often ask: Should I build wealth through mutual funds or invest directly in stocks?

Let’s break this down in simple terms.

The Big Picture: India’s Rising Investment Culture

Only ten years ago, total mutual fund assets under management (AUM) were less than ₹13.17 trillion, and within 36 months, in July 2025, the same number represented by AMFI more than doubled to ₹77 trillion. From this, we can infer two important takeaways:

the asset management industry has matured, developing multiple product offerings,

household investments in SIP’s have become part of the Indian congregate culture.

Mutual funds are no longer niche or exotic; they are mainstream for India’s middle class. Meanwhile, direct stock investing is taking root. Internet brokerages, zero-commission trading models, and greater financial literacy mean that anyone can potentially invest directly in stocks.

Post-COVID Momentum

The pandemic represented a significant watershed moment. Between March 2020 and November 2024:

An increasing depth in equities culture is demonstrated by the nearly threefold increase in mutual fund AUM, which went from ₹22 lakh crore (or ₹22 trillion) to roughly ₹68 lakh crore.

SIP AUM jumped from about ₹2 lakh crore to ₹13 lakh crore

Average monthly SIP inflows increased to $2.7 billion (which is about ₹22,000+ crore) by 2024

Despite the volatile markets, this post-COVID migration to the equity markets shows that people are becoming more confident in risk-taking and disciplined equity trading.

Gender Differences in Investing

Women’s engagement in mutual funds is rapid:

The share of women in individual MF investors rose to 26% in FY25 (vs. 24% previous year)

Women’s AUM doubled over the 5-years (2019-2024), moving from ₹4.59 lakh crore to ₹11.25 lakh crore

Women hold around 33% of the individual investors’ AUM

The adoption rate for women was 319%, and they controlled over 30.5% of the total SIP AUM.

Women’s average SIP ticket size was 22% larger than men’s compared to 45% larger in terms of average lumpsum investment.

Some states and regions are remarkably noteworthy:

Women’s share and mutual fund AUM surpass 33% in at least 13 states and union territories (such as Gujarat, Maharashtra, West Bengal, MP, and Delhi).

All this information emphasizes that women (especially outside of the big metros) are becoming an increasingly important and sophisticated group of investors in India’s investment landscape.

What Exactly Are Mutual Funds and Direct Equity?

Mutual Funds: Investment tools are professionally managed funds where your money is combined with money from other investors. Together this money is used to buy stocks, bonds or a mix of both. Fund managers are in charge of choosing stocks, overseeing the portfolio, and rebalancing it as needed for equity mutual funds. Investors have the option of making systematic SIP investments or making lump sum investments.

Direct Equity: Investing directly in the stocks of companies listed on stock exchanges like NSE or BSE. The investor buys shares based on his/her own research, market timing, or perhaps the suggestion of a third party and then holds or sells the shares. Earning money can be profitable, however, the responsibility to act as base/primary research is with the investor.

Performance: What Does the Data Say?

Here’s where things get interesting.

Mutual Funds: Evidence of Consistency

FinEdge (2025) reports that long-term SIP returns in India averaged between 12% and 15% each year. For example if someone invests ₹10 000 every month in the Bandhan Large & Mid Cap Fund for 20 years the total amount grows to ₹1.15 crore (The Economic Times August 2025). During this time more than sixty equity funds were created that turned people into ‘SIP crorepatis.’

This shows how effective it can be to invest regularly in stocks. By consistently putting in the same amount of money and letting it grow over time you can build wealth even when the market goes up and down.

Direct Equity: Higher Upside, Higher Volatility

On the other hand investors who held onto good companies for a long time generally outperformed any mutual fund that has a long history. Investors who put their money into HDFC Bank, Infosys or Reliance Industries early on have seen their investments grow at a rate of 18% to over 20% each year even after considering inflation for the past 20 to 30 years. The investor needs to hold onto their stocks during market ups and downs, avoid selling in a panic and try to identify a successful investment relatively early.

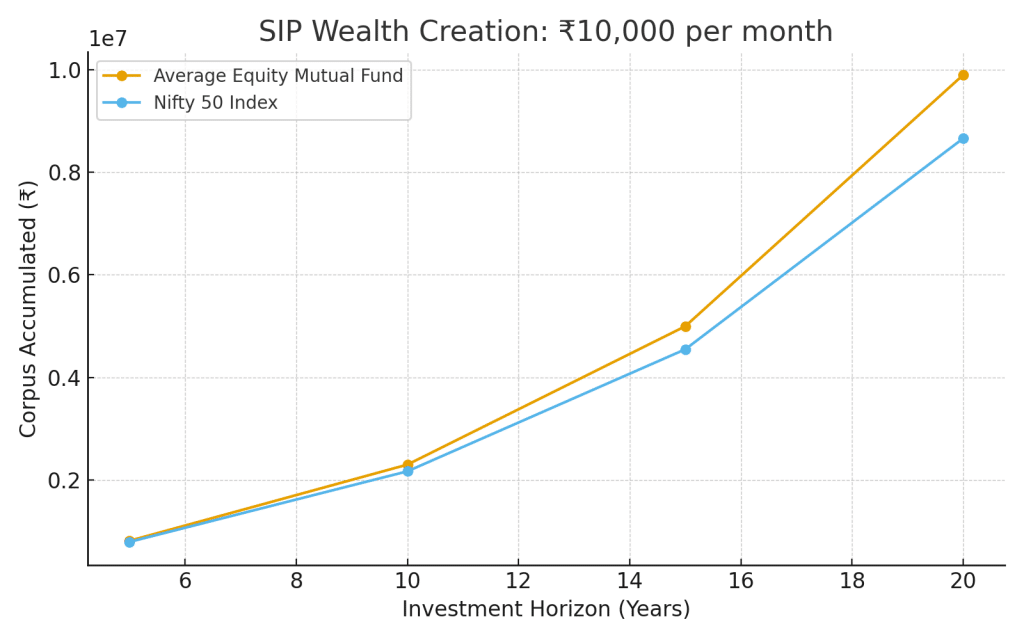

SIP Wealth Creation

X-axis: Investment horizon (5, 10, 15, 20 years)

Y-axis: Corpus accumulated from ₹10,000 monthly SIP

Two lines: Average Equity Mutual Fund vs. Nifty 50 index

Risk and Reward: Comprehending the Trade-offs

1. Mutual Fund Risk

Because they are related to the market, NAVs fluctuate.

Diversification (money spread over 30 to 60 stocks) reduces unsystematic risk.

Less work for stock-pickers equals professional management.

2. Direct equity risk

concentrated exposure in the absence of diversity.

calls for diligent investigation, close observation, and a resilient disposition.

Both multi-bagger gains and significant losses are possible.

According to HSBC’s 2025 research even during tough times the money coming in from Systematic Investment Plans (SIPs) in India remained steady. This shows that individual investors who invest in mutual funds are less likely to leave at the wrong time. On the other hand we have noticed that things like panicking when the market is down, trying to follow trends or selling stocks too quickly often lead to individual stock investors making less money.

Taxation: A Subtle But Important Factor

Mutual Funds: Equity funds receive favorable long-term capital gains (LTCG) tax of 10% when gains exceed ₹1 lakh/year (in the investor’s hand). Distributions as dividends are taxed in the investor’s hands.

Direct Equity: similar LTCG rules apply. However, the more the chatter the quicker gains become short-term (to the tune of 15% tax). This erodes returns.

For investors who are churners direct equity may incur a heavier tax scenario than a long-term SIP.

The Psychological Edge of SIPs

Why are SIPs so popular?

Because they automate discipline. When an investor sets a monthly debit amount, he (or she) must acquire units at different highs and lows consistently, thereby reducing costs by averaging.

The Economic Times (2025) reported that SIP monthly inflows were presently above ₹20,000 crore, suggesting retail investors are more confident in participating in this form of investment. Franklin Templeton India states that retail investors now provide one in every four rupees of mutual fund AUM.

Direct Equity: The Case for Control

SIPs instill discipline, and direct equity makes you in control, as investors can:

Choose companies they believe in.

Change their portfolios in a flash.

Research to go after higher alpha.

However,this requires a lot of time understanding and mental equilibrium. Many beginners will discover that it takes a lot of effort to learn.

That said, successful direct equity investors consistently point out that no mutual fund has done what the patient holder of Infosys since the 1990s and Reliance over the last 20 years has received in returns.

Global and Indian Evidence: Do Mutual Funds or Stocks Win

Research consistently demonstrates across the globe that while global equity indices will produce significant returns over long horizons, the vast majority of active retail investors will underperform due to timing errors.

In India, AMFI data show that SIP mutual funds investors are more likely to retain their investments for longer periods compared to retail equity traders. Although Mutual Funds generated less absolute and less volatility returns for the average household investor over a 10 – 15 year period, it is also true that direct equity has no equal for wealth creation for those who can find winners and hold onto them.

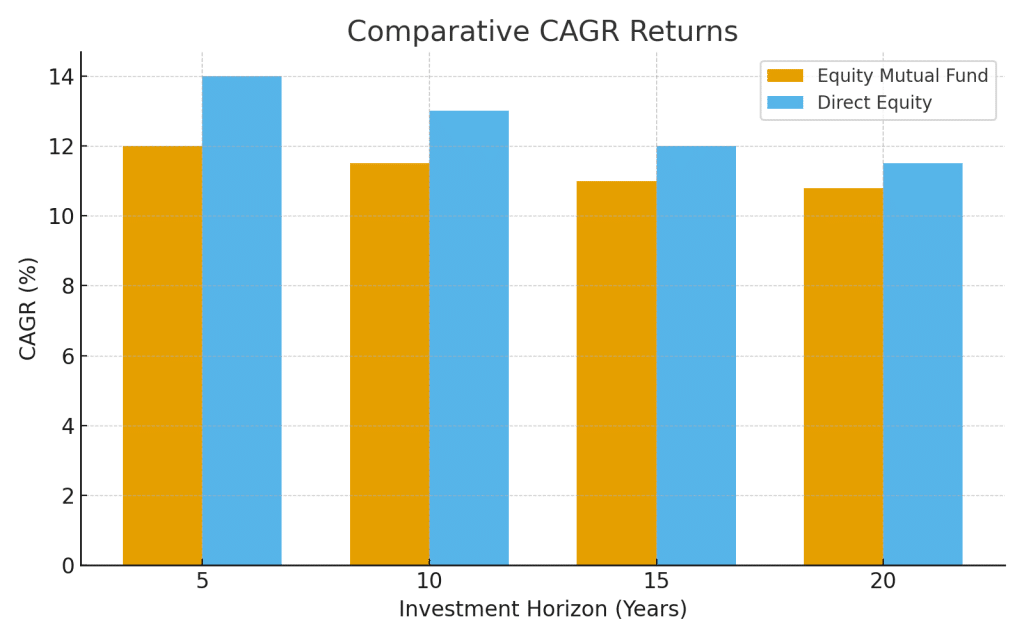

Comparative CAGR Returns

X-axis: 5, 10, 15, 20 years

Y-axis: CAGR (%)

Bars: Average Equity Mutual Fund vs. Direct Equity (Nifty 50 proxy vs. select top stocks)

RMoney’s Perspective

RMoney explains that this hasn’t been so much a debate about who is the winner between mutual funds and direct equity. It is more about aligning the right strategy with the right investor. For new investors or the busy professional, direct mutual funds can be a low-cost, disciplined way to build wealth over time. For investors who are willing to research, are patient, and/or have a high-risk appetite, direct equity has the potential for higher upside. RMoney believes the best approach will be a mix of both strategies, including mutual funds where investors feel they need more stability and direct equity for long-term growth.

Conclusion: Which Builds Wealth Faster?

Mutual Funds: Good for stable, inflation-beating returns with lower effort. Appropriate for most households.

Direct Equity: Good for those willing to do research, concentrate risk, and invest for decades.

We at RMoney understand making wealth is not “either.or.” It’s discovering equilibrium which is appropriate for your personal objectives and targets. If mutual fund stability or direct equity growth is your choice, our team professionals will work within your investment style and risk tolerance and create a portfolio appropriate for you.

Building wealth is not a function of haste. It’s a function of consistent behavior managing risk applications appropriate to the goal.

Disclaimer: This blog is for informational purposes only and should not be considered investment advice. Please consult a SEBI-registered financial advisor before making any investment decisions.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Journey

Tracing our growth and milestones over time.

Journey

Tracing our growth and milestones over time.

Mission & Vision

Guided by purpose, driven by long-term vision.

Mission & Vision

Guided by purpose, driven by long-term vision.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Management

Experienced leadership driving strategic financial excellence.

Management

Experienced leadership driving strategic financial excellence.

Credentials

Certified expertise with trusted industry recognition.

Credentials

Certified expertise with trusted industry recognition.

Press Release

Latest company news, updates, and announcements.

Press Release

Latest company news, updates, and announcements.

Testimonials

Real client stories sharing their success journeys.

Testimonials

Real client stories sharing their success journeys.

7 Reasons to Invest

Top benefits that make investing with us smart.

7 Reasons to Invest

Top benefits that make investing with us smart.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

Our Technology

Advanced tools enabling efficient online trading.

Our Technology

Advanced tools enabling efficient online trading.

Blog

Stay updated with expert insights, market trends, and trading strategies through our informative blogs.

Blog

Stay updated with expert insights, market trends, and trading strategies through our informative blogs.

Video

Learn visually with easy-to-understand videos covering trading concepts, tips, and market analysis.

Video

Learn visually with easy-to-understand videos covering trading concepts, tips, and market analysis.

Podcast

Tune in to insightful discussions and expert opinions anytime, anywhere.

Podcast

Tune in to insightful discussions and expert opinions anytime, anywhere.

Telegram Community

Be part of an active trader community sharing ideas, updates, and market opportunities in real-time.

Telegram Community

Be part of an active trader community sharing ideas, updates, and market opportunities in real-time.

WhatsApp Updates

Get instant alerts, key market updates, and important notifications directly on WhatsApp.

WhatsApp Updates

Get instant alerts, key market updates, and important notifications directly on WhatsApp.

Financial Calculators

Plan your trades, margins, and returns efficiently with our smart calculation tools.

Financial Calculators

Plan your trades, margins, and returns efficiently with our smart calculation tools.

Marketplace

Discover curated tools, strategies, and services designed to enhance your trading experience.

Marketplace

Discover curated tools, strategies, and services designed to enhance your trading experience.

Feedback

Share your suggestions or concerns to help us improve your experience.

Feedback

Share your suggestions or concerns to help us improve your experience.

Downloads

Access important forms, software, and documents in one place.

Downloads

Access important forms, software, and documents in one place.

Locate Us

Find the nearest RMoney branch or service center quickly.

Locate Us

Find the nearest RMoney branch or service center quickly.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Account Modification

Update personal or bank details linked to your trading account.

Account Modification

Update personal or bank details linked to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.

Authorised Person Partner with us as an Authorised Person to grow your financial business.

Authorised Person Partner with us as an Authorised Person to grow your financial business.

Refer & Earn

Invite friends and earn rewards every time they trade with us.

Refer & Earn

Invite friends and earn rewards every time they trade with us.