Natural Gas 2025: From Shale Boom to Global Power Driver

Published : December 4, 2025

Natural gas is one of the most volatile and dynamic commodities on the market. Natural Gas prices are driven by factors as simple as a temperature forecast or as complex as global geopolitics.

The Multi Commodity Exchange (MCX) initiated natural gas financial trading in India in 2015 with cash-settled futures contracts, primarily benchmarked to the US Henry Hub price, and used solely for hedging and speculation. This financial market existed without physical settlement until the launch of the Indian Gas Exchange (IGX), which established India’s first nationwide online platform for physical, delivery-based gas trading.

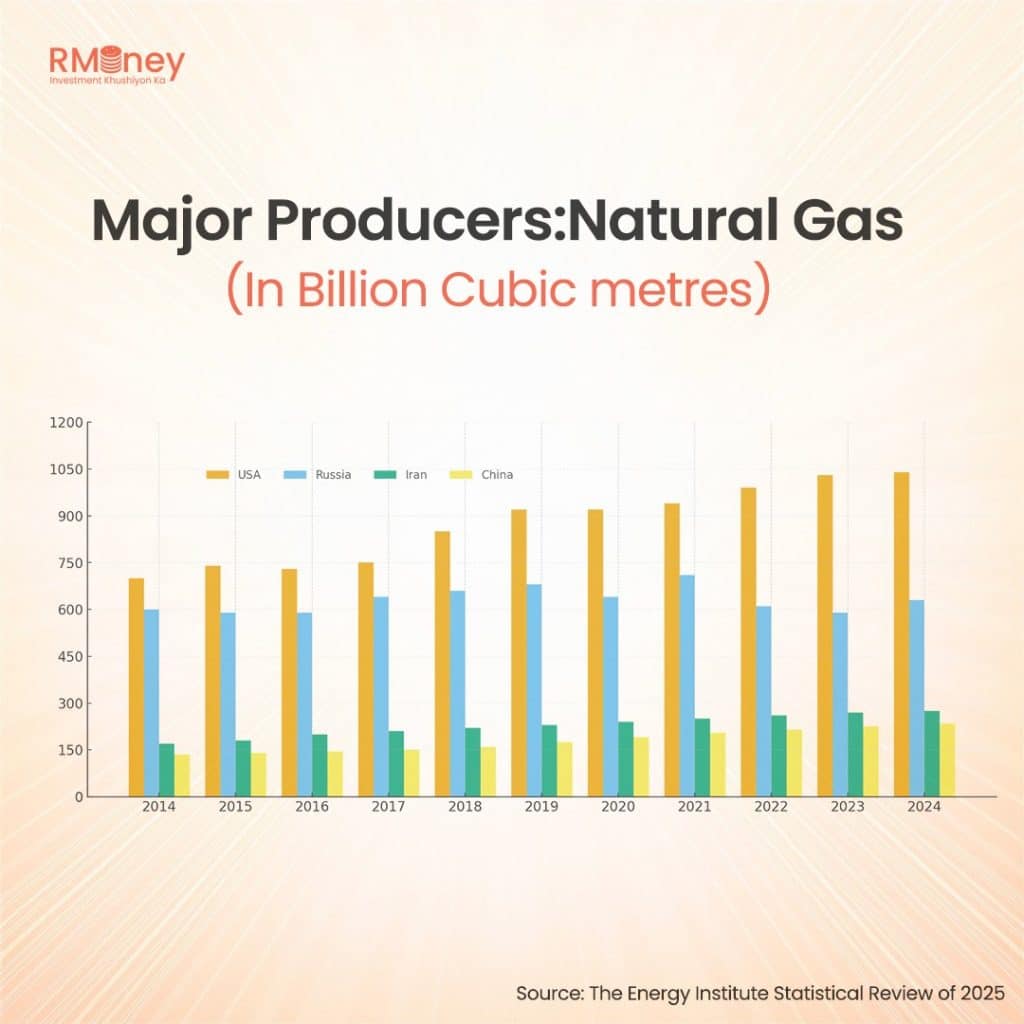

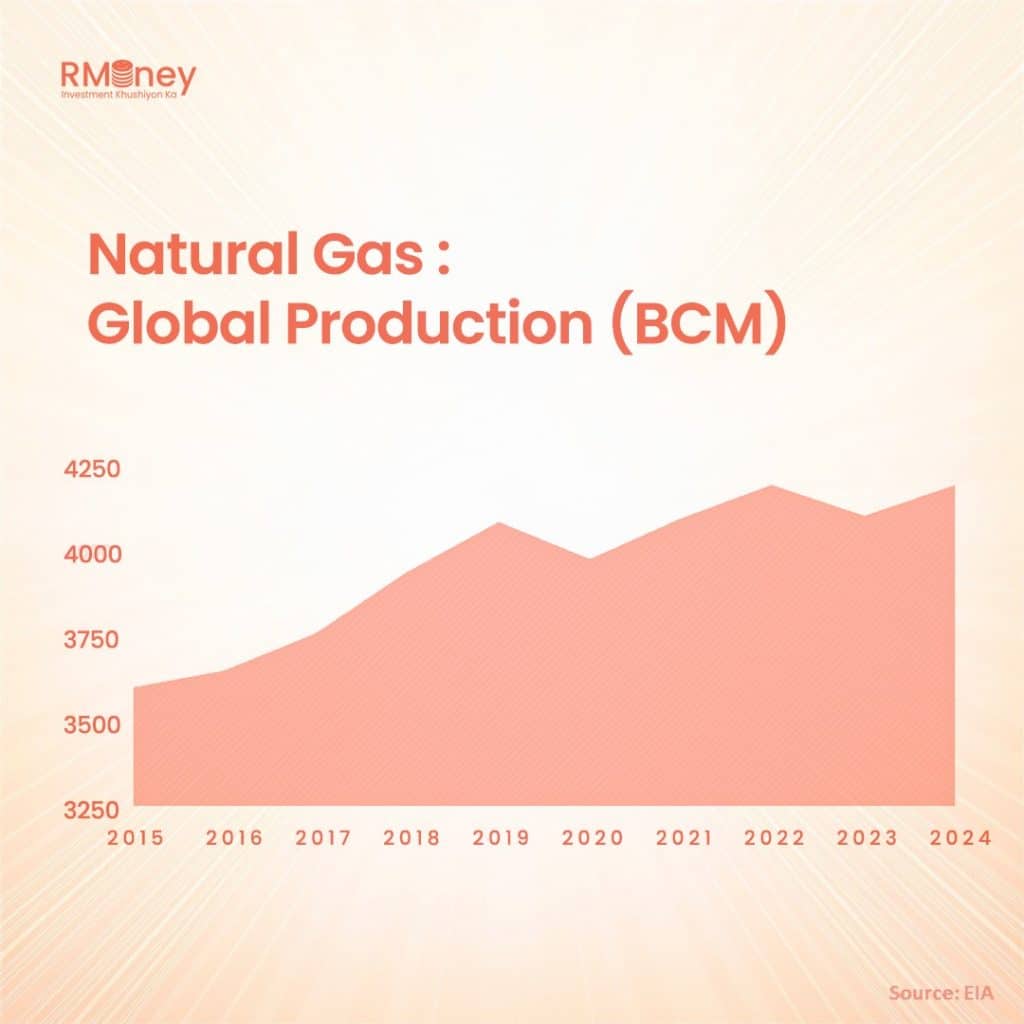

Global natural gas production has demonstrated significant resilience and a strong long-term upward trajectory, rising from around 3,600 Bcm in 2015 to over 4,200 Bcm in 2024. While output briefly faltered during the 2020 COVID-19 disruption and saw a minor dip in 2023, the market quickly recovered. This stability highlights a growing global reliance on gas and was achieved as increased supply from key producers like the US and Norway offset declines, particularly from Russia, due to geopolitical events. The Energy Institute confirmed this recent strength, reporting a 1.2% rise in 2024 to 4,124 Bcm. Crucially, the United States, Russia, Iran, and China collectively account for 53% of the world’s natural gas supply.

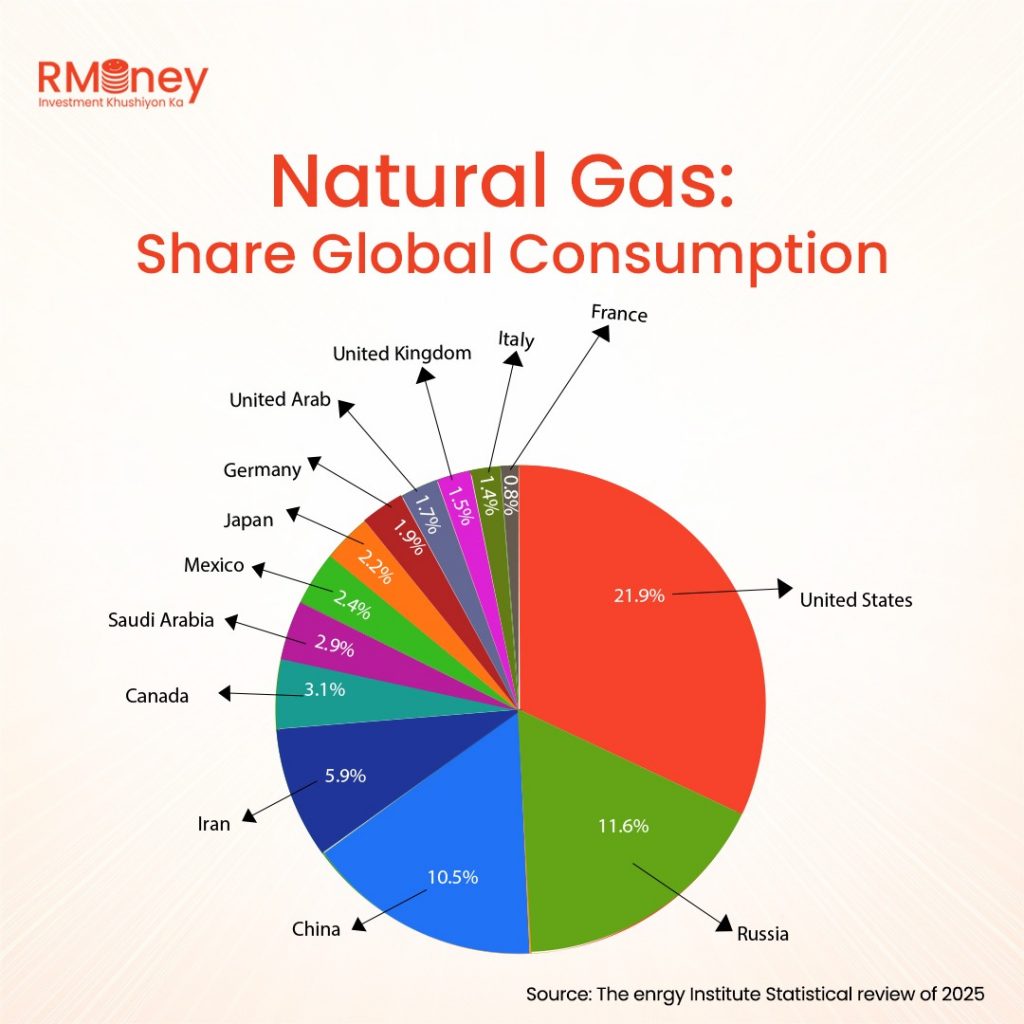

While global natural gas consumption spiked significantly in 2024, far exceeding the 2% average annual growth rate seen from 2010 to 2020 (driven primarily by Asia, especially China, and the switch from coal/oil in electricity), the growth trajectory is now slowing. Preliminary 2025 data shows consumption rose by only about 0.5% year-on-year, a sharp deceleration from 2.8% growth in 2024 to an expected full-year rise of less than 1%. This subdued 2025 growth was almost entirely confined to Europe and North America, as demand weakened in Asia Pacific (expanding by less than 1%, the slowest rate since 2022) and declined in Eurasia. Despite these shifts, the United States remains the world’s largest consumer, accounting for 21.9% of global gas use.

US: NATURAL GAS STORY

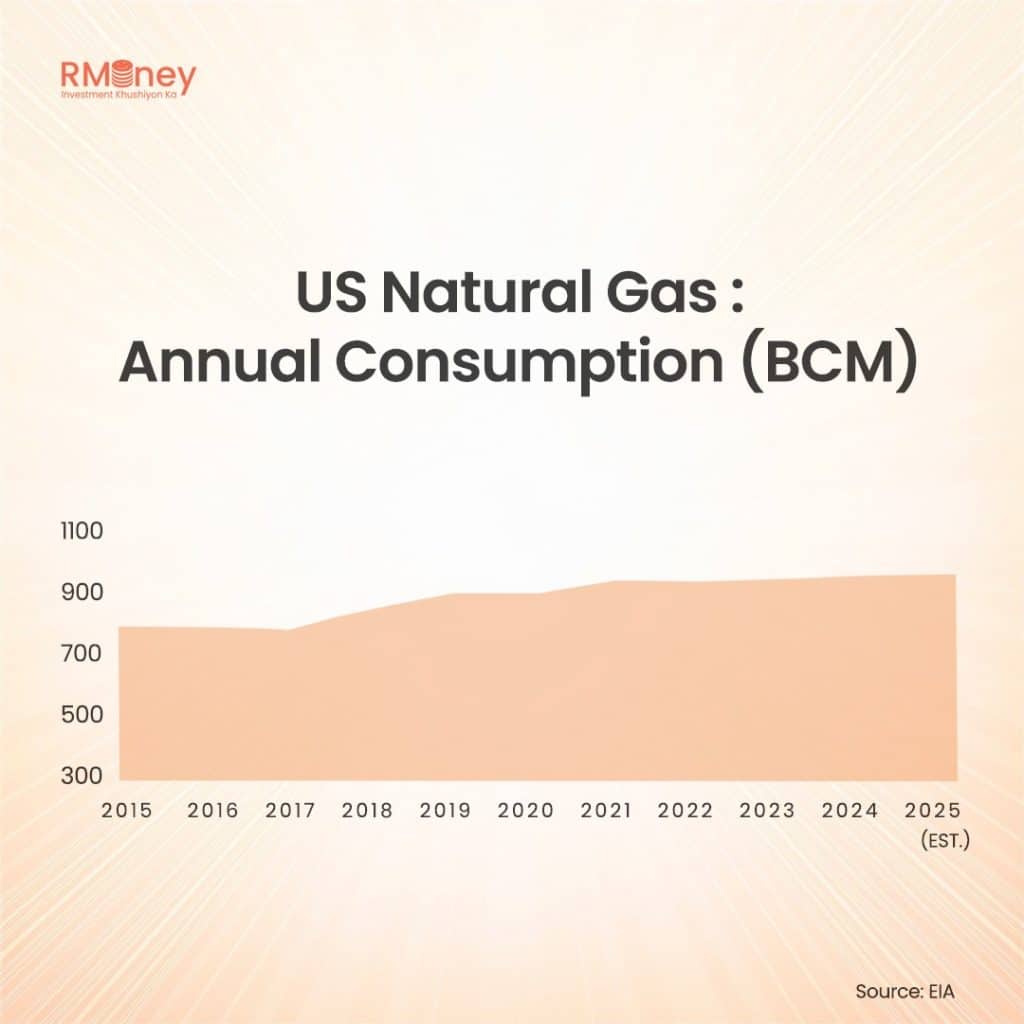

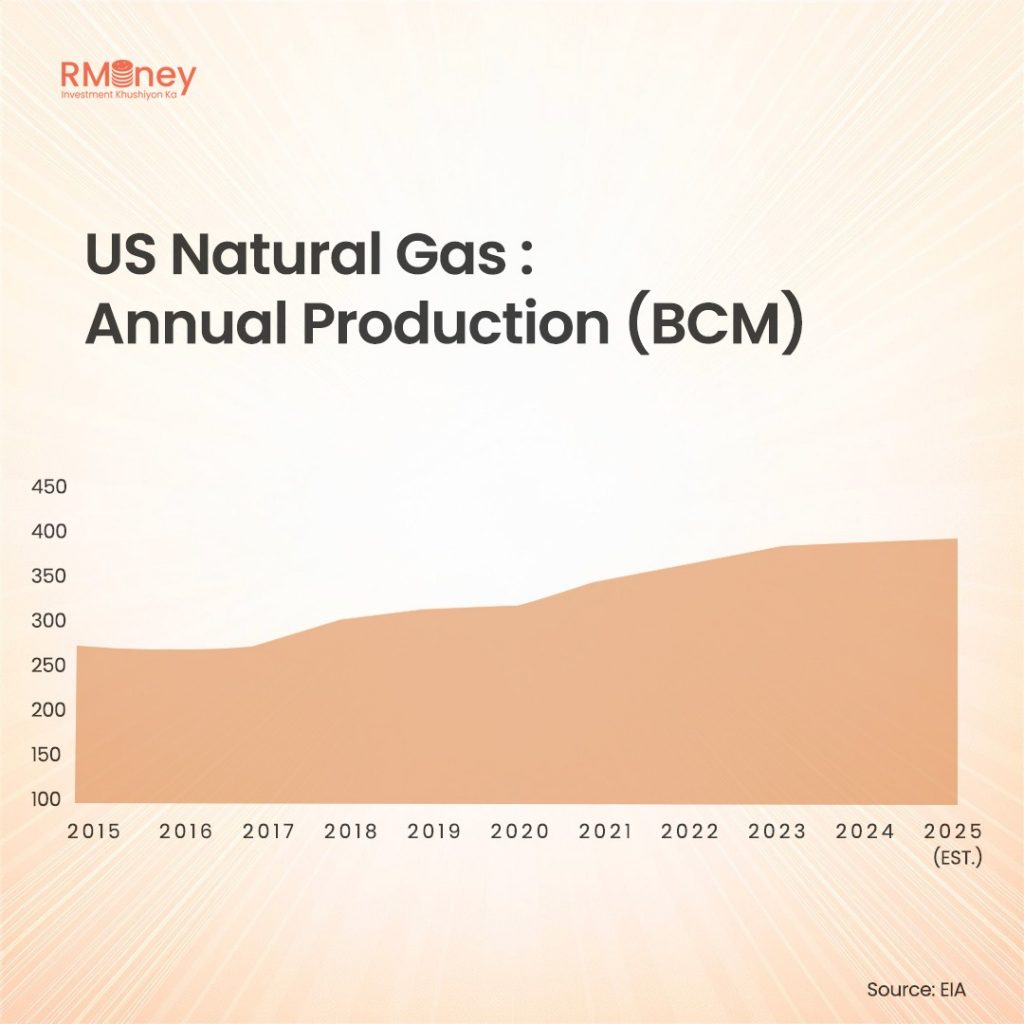

The US natural gas market prior to the shale boom, which began commercially in the early 2000s, was characterized by two defining trends: a structural decline in domestic output and growing import dependence. Following a peak in production around 1973, US gas extraction entered a prolonged slump as conventional reservoirs matured, causing production to stagnate at around 18-19 trillion cubic feet (Tcf) through the 1990s and early 2000s. This shortage led the US to become a significant net importer of natural gas, relying heavily on Canadian pipeline supply and planning costly infrastructure for imported Liquefied Natural Gas (LNG), creating widespread concern over long-term energy security and domestic supply constraints.

SHALE GAS BOOM

The widespread application of fracking and horizontal drilling triggered the Shale Gas Boom, (started in the early to mid-2000s, achieving commercial viability around 1998) dramatically altering the US energy landscape. This revolution propelled the US past Russia to become the world’s largest natural gas producer and transformed it from a net importer to a key exporter, with shale gas now accounting for approximately 78% of domestic production. This dominance, however, is now challenged by maturity headwinds. Economically, the industry is navigating rising costs and less productive drilling locations, necessitating a focus on shareholder returns over growth and driving consolidation. Operationally, producers face intensified environmental and regulatory pressures concerning stringent methane emission reductions and sustainable water management. Despite the geopolitical benefits of its massive export capacity, the US domestic gas market is increasingly sensitive to global price fluctuations and continues to struggle with regional pipeline constraints.

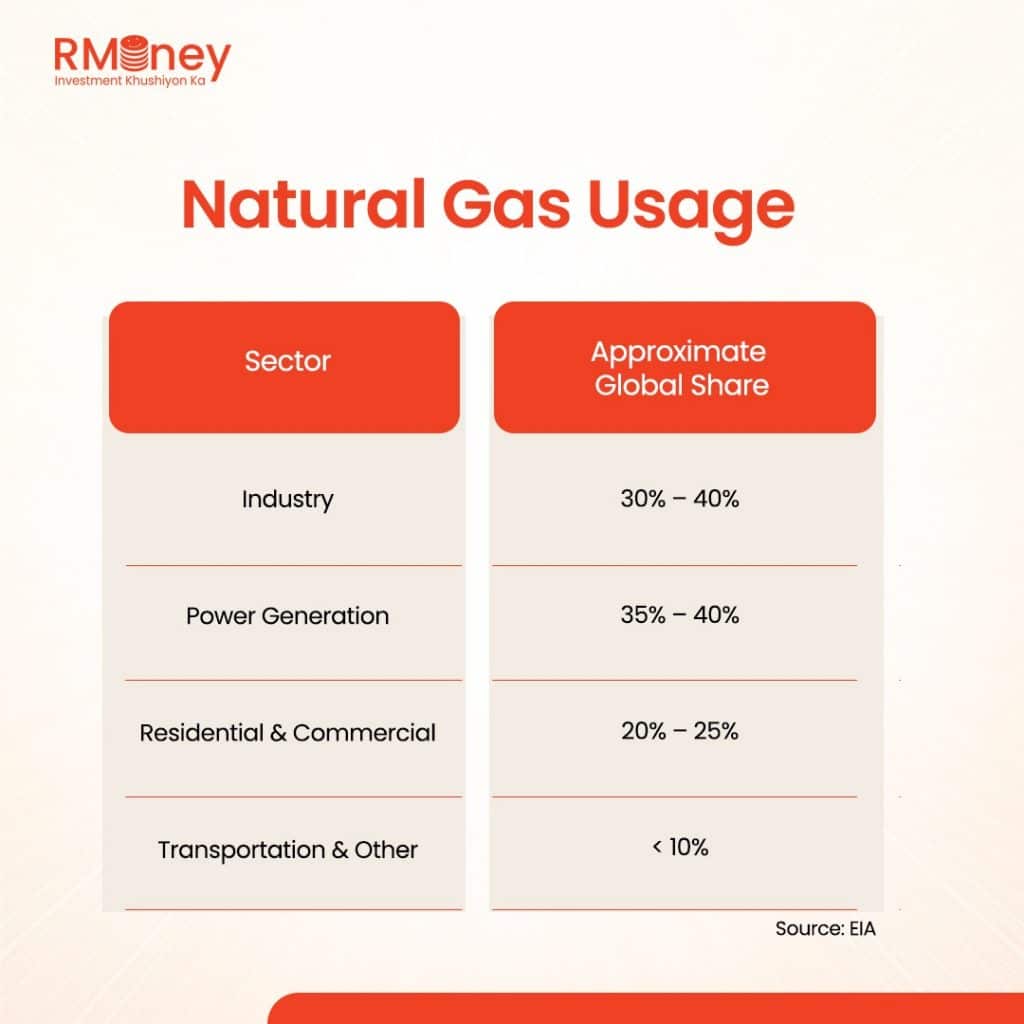

WHERE ALL DOES NATURAL GAS GO?

Far exceeding its use in heating homes and businesses, natural gas functions as the key driver for global power and industry. Around 35% to 40% of consumption is dedicated to generating electricity, where gas serves as the cleaner alternative to coal and provides the essential flexibility needed to integrate wind and solar power. Almost as much, 30% to 40%, is consumed by the industrial sector, where it performs dual roles: as a fuel for intensive heating processes (such as cement and steel production) and as the indispensable raw material (feedstock) for manufacturing vital products like plastics and fertilizers. Thus, the majority of global gas consumption is centralized in factories and power plants, supporting both industrial growth and the global energy transition.

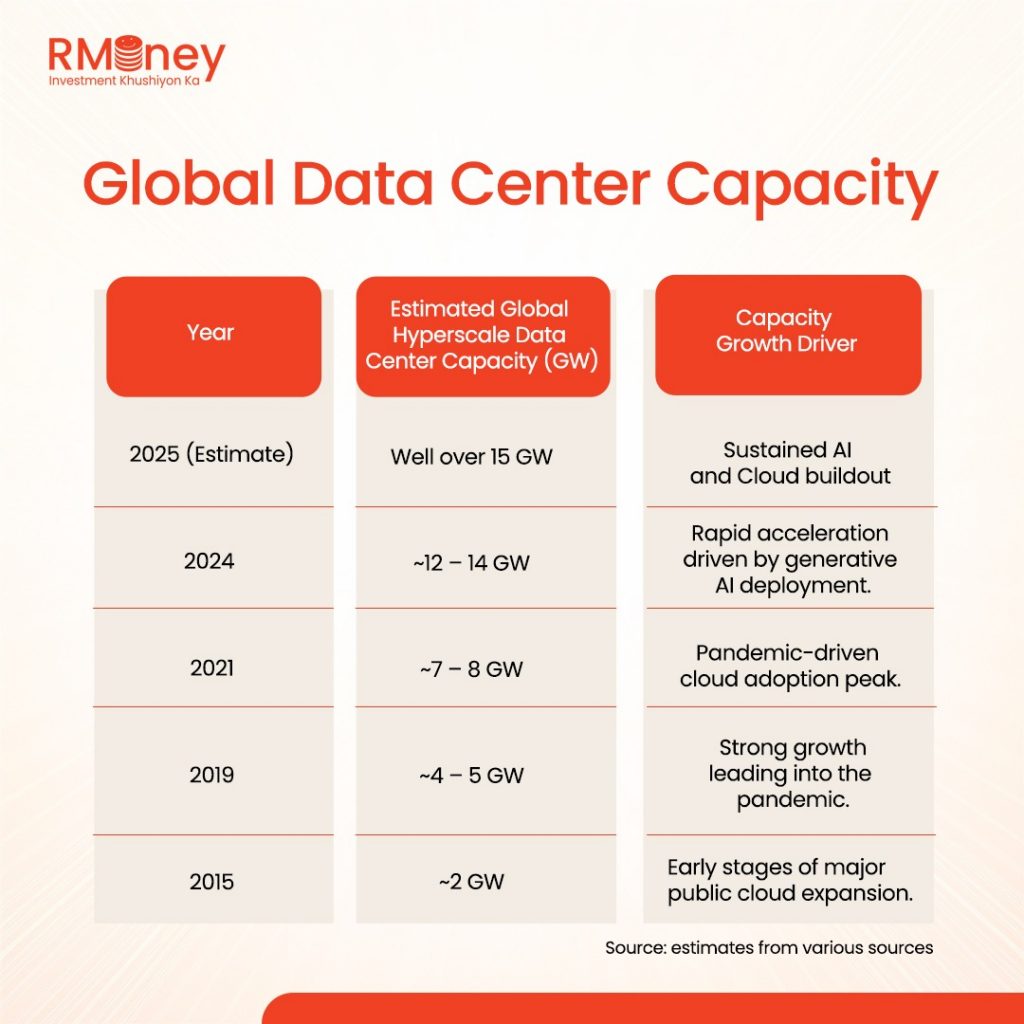

RISE OF DATA CENTRE AND USAGE OF NATURAL GAS

The digital world runs on data centers, and those massive energy warehouses are driving a new surge in global natural gas demand. The explosion of AI and cloud computing requires continuous, reliable power, which gas-fired plants are uniquely positioned to provide. Furthermore, gas solidifies its role through the use of on-site natural gas generators—the essential backup required by major operators to guarantee zero downtime. As data consumption shows no signs of slowing, natural gas has become the indispensable energy partner sustaining the relentless growth of the digital revolution.

GLOBAL PRICE BENCHMARK: HENERY HUB, TTF and JKM

North America’s key natural gas price, the Henry Hub, has evolved from a regional benchmark to a global anchor. Following its establishment after the deregulation of the 1990s, the Hub experienced extreme volatility driven by a perceived scarcity. However, the market fundamentally shifted after 2016 with the commissioning of US LNG export terminals. This infrastructure tethered Henry Hub to international markets, transforming its price from a purely domestic metric into one that reflects the delicate balance between abundant US supply (thanks to shale) and the powerful pull of volatile global demand, positioning it as a crucial reference point for the world’s gas trade.

Created in 2003, the Dutch Title Transfer Facility (TTF) began as a simple trading point. Yet, thanks to its superior infrastructure and central position connecting major European pipelines, it rapidly became the continent’s premier gas hub. The TTF’s dominance marked the end of outdated oil-indexed pricing, ushering in competitive “gas-on-gas” market forces. Now, its price is the essential, volatile heartbeat of European energy security, immediately reacting to changes in gas storage, extreme weather, and geopolitical tensions to set prices for millions of homes and businesses.

Japan Korea Marker (JKM) determines the price of LNG for the world’s biggest gas consumers in Northeast Asia. Published daily by Platts and quoted in $/MMBtu, the JKM is a powerful price assessment based on actual spot LNG trades delivered to nations like Japan, Korea, and China. By replacing outdated oil-indexation, the JKM now functions as Asia’s primary reference for gas contracts. Its fluctuations are a vital signal, acting as the essential barometer for the entire Asian LNG market and playing a key role in driving global gas price volatility.

INDIA: NATURAL GAS STORY

India is embarking on a significant energy transition that will see its natural gas demand increase by nearly 60% by 2030, reaching an annual consumption of 103 bcm, according to the IEA. This massive growth is thanks to new infrastructure and local production efforts. Domestic supply is only expected to hit 38 bcm, meaning India will have to more than double its LNG imports, to about 65 bcm, making it one of the most critical buyers in the global gas market this decade.

India is aiming for a huge clean energy transition! The Government of India has laid down a highly ambitious goal to dramatically increase the role of natural gas in the country’s energy consumption. They plan to boost gas’s share in the total energy mix from the 2022 level of just 6.4% to a formidable 15% by 2030. This target is not just a modest bump; it represents more than doubling the fuel’s contribution in less than a decade, positioning gas as a critical ‘bridge fuel’ for cleaner air and industrial growth.

DECODING THE ANNUAL NATURAL GAS STORAGE CYCLE

At the Henry Hub, US natural gas pricing is primarily dictated by the weather forecast and the ensuing market expectations. The cycle begins with winter (December-March): prolonged cold snaps heating degree days (high HDDs) create urgent heating demand, pushing prices bullish as massive storage withdrawals are expected. The lowest prices appear in the spring “shoulder season” (April–May) during the injection period’s start. Demand peaks again in summer as extreme heat Cooling Degree Days (high CDDs) drives up power generation needs, causing price rallies even as injections continue. The autumn shoulder season concludes injections, setting the final inventory level and risk premium for the coming winter. Ultimately, the market is a reaction machine: traders use weather models to forecast the EIA Storage Report, and any surprise in the actual weekly draw or injection triggers an immediate, definitive price swing.

CURRENT FACTORS AFFECTING NATURAL GAS

Despite a near-record supply forecast—the EIA projects 2025 US production at a massive 107.67 bcf/day, natural gas prices are surging to multi-month highs on both MCX (₹432.8) and global exchanges. The simple reason is the demand acceleration. The near-term trigger is a massive, weather-driven spike, with forecasts predicting a cold snap in the US Northeast that is rapidly increasing heating expectations. This spike is amplified by a structural surge in electricity use; the EEI reported US output climbed 5.33% year-over-year for the week ending November 15. The bottom line: record US production is being outpaced by a dual-threat of demand—seasonal heating plus the continuous, massive energy hunger of AI and data centers, making the US supply anchor insufficient to tame global volatility.

Disclaimer: The information provided in this blog is for informational and educational purposes only and should not be construed as financial, investment, or trading advice. Natural gas markets are highly volatile, and prices can fluctuate due to multiple factors, including geopolitical events, weather patterns, and market dynamics. Readers should conduct their own research and consult with a licensed financial advisor before making any investment or trading decisions. RMoney is not responsible for any losses or damages that may arise from the use of this information.

Moumita Samanta is a Senior Fundamental Research Analyst at Rmoney, bringing a unique and powerful combination of financial market acumen and specialized industry expertise to our research team. With over seven years of experience as a fundamental analyst, Moumita has cultivated a deep understanding of investment dynamics across both the equity and commodity markets, previously contributing to the success of organizations like SS wealthStreet, Advisorymadi.com, and Globe Capital.

What truly sets Moumita apart is her extensive 12-year background in the bullion market and the gems and jewellery industry. This hands-on, sector-specific knowledge provides an invaluable perspective, particularly when analyzing commodity-linked assets and luxury retail segments.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Stock Trading

Now trade in ₹9 Per Order or ₹ 999 Per Month Plans.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Future & Options

Access F&O contracts with advanced tools for hedging and speculation.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Currency Trading

Trade in major currency pairs and manage forex exposure efficiently.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Commodity Trading

Diversify Trading with MCX & NCDEX by Trading in Gold, Silver, Base Metals, Energy, and Agri Products.

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Margin Trading Funding

Boost your buying power with upto 5X, Buy now Pay Later

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Algo Trading

Back test, Paper Trade your logic & Automate your strategies with low-latency APIs.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Trading View

Leverage Trading View charts and indicators integrated into your trading platform.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Advanced Options Trading

Execute multi-leg option strategies with precision and insights.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Stock Lending & Borrowing

Earn passive income by lending stocks securely through SLB.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

Foreign Portfolio Investment

Enable NRIs and FPIs to invest in Indian markets with ease and compliance.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

IPO

Invest in upcoming IPOs online with real-time tracking and instant allotment updates.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Direct Mutual Funds

0% Commissions by investing in more than +3500 Direct Mutual Fund Scheme.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Corporate FDRs

Earn fixed returns with low-risk investments in high-rated corporate fixed deposits.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Stocks SIPs

Build long-term wealth with systematic investment plans in top-performing stocks.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Bonds & NCDs

Access secure, fixed-income investments through government and corporate bond offerings.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Depository Services

Safely hold and manage your securities with seamless Demat and DP services with CDSL.

Journey

Tracing our growth and milestones over time.

Journey

Tracing our growth and milestones over time.

Mission & Vision

Guided by purpose, driven by long-term vision.

Mission & Vision

Guided by purpose, driven by long-term vision.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Why RMoney Platform

Smart, reliable platform for all investors' needs.

Management

Experienced leadership driving strategic financial excellence.

Management

Experienced leadership driving strategic financial excellence.

Credentials

Certified expertise with trusted industry recognition.

Credentials

Certified expertise with trusted industry recognition.

Press Release

Latest company news, updates, and announcements.

Press Release

Latest company news, updates, and announcements.

Testimonials

Real client stories sharing their success journeys.

Testimonials

Real client stories sharing their success journeys.

7 Reasons to Invest

Top benefits that make investing with us smart.

7 Reasons to Invest

Top benefits that make investing with us smart.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

SEBI Registered Research

Trusted insights backed by SEBI-compliant research.

Our Technology

Advanced tools enabling efficient online trading.

Our Technology

Advanced tools enabling efficient online trading.

Calculators

Access a suite of smart tools to plan trades, margins, and returns effectively.

Calculators

Access a suite of smart tools to plan trades, margins, and returns effectively.

Margin Calculator

Instantly check margin requirements for intraday and delivery trades.

Margin Calculator

Instantly check margin requirements for intraday and delivery trades.

MTF Calculator

Calculate MTF funding cost upfront to ensure full transparency before placing a trade.

MTF Calculator

Calculate MTF funding cost upfront to ensure full transparency before placing a trade.

Brokerage Calculator

Know your exact brokerage charges before placing any trade.

Brokerage Calculator

Know your exact brokerage charges before placing any trade.

Market Place

Explore curated investment products and trading tools in one convenient hub.

Market Place

Explore curated investment products and trading tools in one convenient hub.

RMoney Gyan

Enhance your market knowledge with expert blogs, videos, and tutorials.

RMoney Gyan

Enhance your market knowledge with expert blogs, videos, and tutorials.

Performance Tracker

Track our research performance with full transparency using our performance tracker.

Performance Tracker

Track our research performance with full transparency using our performance tracker.

Feedback

Share your suggestions or concerns to help us improve your experience.

Feedback

Share your suggestions or concerns to help us improve your experience.

Downloads

Access important forms, software, and documents in one place.

Downloads

Access important forms, software, and documents in one place.

Locate Us

Find the nearest RMoney branch or service center quickly.

Locate Us

Find the nearest RMoney branch or service center quickly.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Escalation Matrix

Resolve issues faster with our structured support escalation process.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Back Office

Log in to view trade reports, ledger, and portfolio statements anytime.

Account Modification

Update personal or bank details linked to your trading account.

Account Modification

Update personal or bank details linked to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Fund Transfer

Transfer funds instantly online with quick limit updation to your trading account.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

Bank Details

View our registered bank account details for seamless transactions by NEFT, RTGS or IMPS.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick Mobile App

Trade on-the-go with our all-in-one mobile trading app.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Quick login

Quickly access your trading account through the RMoney Quick web-based trading.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Web Version

Experience powerful web-based trading with advanced tools for algo traders.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.

RMoney Rocket Mobile Version

Trade anytime, anywhere with our feature-rich mobile trading platform.